Goldman повысил оценку поставок Tesla и улучшил настроение бренда

Аналитики Уолл-стрит преследуют акции Tesla, поскольку они торгуются выше 400 долларов за акцию, после новостей о том, что Илон Маск купил акции на сумму 1 миллиард долларов, чтобы начать неделю.

Забегая вперед, отчет о поставках Tesla в третьем квартале ожидается менее чем через две недели. Аналитики Goldman повысили оценки поставок и целевые цены. Данные Goldman Sachs также показывают Настроения вокруг Tesla улучшились После падения в начале этого года, когда финансируемая за темные деньги машина НПО Демократической партии вела войну против Маска за его усилия DOGE.

Члены Социалистической стрелковой ассоциации были обвинены в нападении на объект ICE в Альваредо, штат Техас, в котором полицейский был застрелен в шею, и в двух бомбардировках дилерских центров Tesla (политические атаки против @elonmusk). Другой присоединился к иностранной террористической организации. pic.twitter.com/StMPgjQtRS

— Luke Rosiak (@lukerosiak) 18 сентября 2025 г.

Команда аналитиков во главе с Марком Делани Обновлены оценки поставок автомобилей Tesla в третьем и четвертом кварталах:

3Q25: 455K (предыдущее 430K; консенсус 439K)

4Q25: 450K (предыдущее 443K; консенсус 441K)

2026: без изменений при 1,865 М, в соответствии с консенсусом

""Мы приписываем лучшие объемы 2H частично недавнему запуску модели Y L, частично на основе несколько лучших данных опроса потребителей, а частично с кредитами на покупку IRA EV, срок действия которых истекает 30.09.25.— написал Делейни в записке к клиентам.

Даже с обновленными ежеквартальными оценками поставок команда Делани поддерживает «нейтральный» рейтинг акций. Однако они Они повысили свою 12-месячную целевую цену до $395 с $300.. Вот объяснение:

Мы остаемся нейтральными по отношению к акциям. В долгосрочной перспективе мы Tesla планирует увеличить EPS за счет увеличения вклада автономности и робототехникиХотя наши базовые ожидания прибыли в этих областях более измерены, чем таргетинг компании. Как мы подробно излагаем в этой заметке, мы оцениваем, что его EPS 2030 года может составлять от ~ 2-3 до ~ 20 долларов США (хотя мы признаем, что есть результаты за пределами этих диапазонов), и то, что мы считаем сценарием типа дороги, подразумевает ~ 7-9 долларов США EPS в 2030 году и EPS CAGR ~ 40-50%. Учитывая рост рыночных мультипликаторов в целом, а также темпы роста, которые, по нашему мнению, бизнес может поддерживать в долгосрочной перспективе, а также увеличение прогнозов EPS, мы повышаем наш 12-месячный целевой показатель цены до $395 с $300. Если Tesla может иметь большую долю в таких областях, как гуманоидная робототехника и автономия, то у нас может быть преимущество по сравнению с нашей ценовой целью, хотя если конкуренция ограничивает прибыль (как это происходит с рынком ADAS в Китае) или Tesla не работает хорошо, то может быть и недостаток.

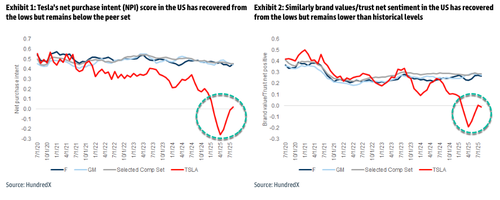

Новые данные опроса потребителей от HundredX и Morning Consult, которые отслеживают намерение покупки и чистый шум вокруг бренда автомобиля. Улучшение настроения. Ранее в этом году НКО, финансируемые Демократической партией, вели информационную войну против Теслы из-за участия Маска в DOGE, но эта пропагандистская кампания утихла много месяцев назад. Потребители возвращаются к бренду.

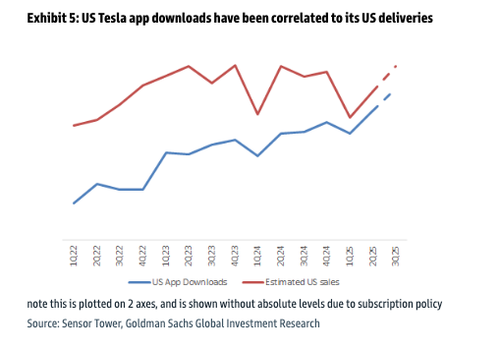

Загрузки приложений также показывают многообещающую точку перегиба Для бренда.

Для полного пакета отчетов и диаграмм ZeroHedge Pro Subs может найти заметку в обычном месте.

Тайлер Дерден

Фри, 09/19/2025 - 13:25