Премьер-министр Японии Ишиба обещает «остаться», несмотря на то, что правящая коалиция столкнется с крупными потерями

Обновление (1015ET): Правящая коалиция премьер-министра Шигеру Исибы Вероятно, потеряет большинство в двух палатах парламента Японии на ключевых выборах в воскресенье.ухудшение политической нестабильности в стране.

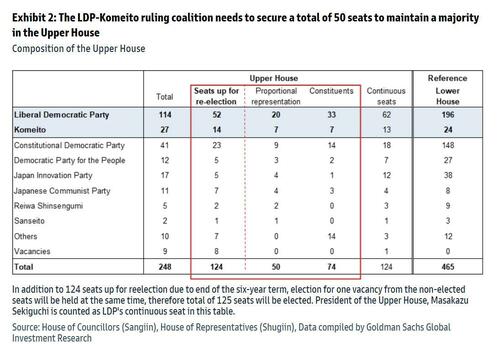

Избиратели выбирали половину из 248 мест в верхней палате, менее влиятельной из двух палат в японской диете.

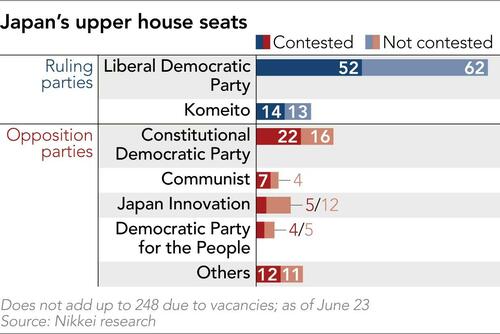

Ishiba установила низкий планку, желая простого большинства в 125 мест. Это означает, что его Либерально-демократическая партия, или ЛДП, и ее младший партнер по коалиции, поддерживаемый буддистами, Комейто должны выиграть 50, чтобы добавить к 75 местам, которые у них уже есть.

Это означало бы большое отступление от 141 места, которое они имели до выборов.

Только ЛДП, по прогнозам, получит от 32 до 35 мест, наименьшее из которых получит партия. Это партия No1 в парламенте.

"Это сложная ситуация. Я принимаю это смиренно и искренне. Исиба рассказал в прямом эфире интервью NHK.

Он сказал, что плохие результаты были связаны с тем, что меры его правительства по борьбе с ростом цен еще не достигли многих людей.

«Я выполню свои обязанности главы партии No 1 и буду работать на страну. "

Сегодняшнее голосование произошло после того, как коалиция Исибы потеряла большинство на октябрьских выборах в нижнюю палату, уязвленная прошлыми коррупционными скандалами, и его непопулярное правительство с тех пор вынуждено идти на уступки оппозиции, чтобы получить законодательство через парламент.

Он не смог быстро принять эффективные меры для смягчения роста цен, включая традиционный основной продукт Японии рис, и сокращение заработной платы.

Потеря контроля над верхней палатой сделает администрацию Исибы первым правительством, возглавляемым ЛДП, которое будет править с меньшинством в обеих палатах парламента. Впервые с момента образования партии в 1950-х годах.

Наконец, как сообщает AP, как мы видели в других регионах по всему миру, Разочарованные избиратели быстро обращаются к новым популистским партиям.

Однако восемь основных оппозиционных групп слишком раздроблены, чтобы создать общую платформу в качестве единого фронта и получить поддержку избирателей в качестве жизнеспособной альтернативы.

Если результаты опроса верны (и, похоже, так и есть), то Сценарий В (ниже) в игре.

** **

Голосование на выборах в верхнюю палату парламента Японии началось в воскресенье в 7 утра по местному времени на более чем 44 000 избирательных участках, в ходе голосования, где борьба с инфляцией и иммиграционной политикой стали ключевыми политическими вопросами, и где кипящее недовольство инфляцией и нерешенные переговоры с США по тарифам могут положить конец карьере премьер-министра Шигеру Исиба.

В общей сложности 125 из 248 мест палаты могут быть избраны, в том числе 50 мест, выделенных пропорциональной представленностью, и одно дополнительное избрание для вакантного места в Токио.

Голосование заканчивается в 8 вечера, а результаты начнут поступать в конце воскресенья и продолжатся в начале утра понедельника. Граждане Японии в возрасте 18 лет и старше имеют право голоса.

Либерально-демократическая партия, которая была правящей партией на протяжении большей части послевоенной истории Японии и партнером по коалиции Комейто. Для поддержания большинства в верхней палате необходимо 50 мест. Но, по данным Nikkei и различных местных СМИ, это выглядит все более сложным, основываясь на недавних опросах.

"" Я не обязательно ищу немедленную смену правительства, но я считаю, что нам нужно больше идей для экономики, чем просто от ЛДП, - сказал Хироясу Кан, 28-летний мужчина в Токио. Он проголосовал за партию, которая, по его мнению, предлагает «конкретные политические предложения». "

Потеряв большинство на выборах в нижнюю палату парламента в октябре прошлого года, правящая коалиция потеряет контроль над парламентом и законодательным процессом. Это приводит к бесчисленным возможным результатам, включая отставку премьер-министра Шигеру Исибы и внеочередные всеобщие выборы, которые могут привести к смене правительства. Это, в свою очередь, приведет к падению курса иены и может иметь серьезные последствия как для японского, так и для мирового рынка облигаций. (См. статью «Приведет ли шок цен на рис в Японии к краху правительства и глобальному кризису облигаций»).

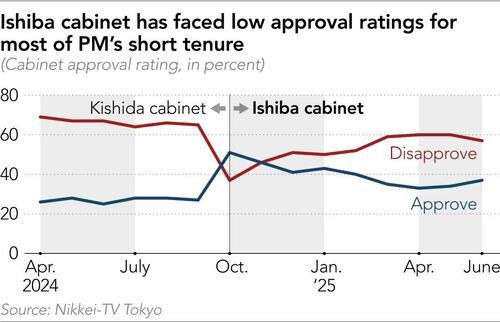

Убыток Исибы, который боролся с низкими рейтингами одобрения на протяжении всего своего короткого срока пребывания в должности, также осложнит торговые переговоры Японии с США, поскольку 1 августа крайний срок, чтобы избежать угрожаемого 25% «взаимного» тарифа, быстро приближается. «Поражение коалиции ЛДП-Комейто может вызвать опасения по поводу отсутствия сделки», — считают экономисты UBS.

В преддверии голосования электорат все больше недоволен растущей инфляцией, особенно для риса, и застойным ростом заработной платы. Основные потребительские цены, которые не включают волатильные цены на свежие продукты питания, но включают рис, который взорвался выше из-за плохого планирования и поставок, выросли на 3,3% в июне по сравнению с годом ранее, выше целевого показателя Банка Японии в 2%.

Выборы — это в некотором смысле соревнование тех, кто может предложить больше «свободного дерьма»: оппозиционные партии получили широкую поддержку. Пропагандируя снижение налога на потребление, Это форма налога на добавленную стоимость (НДС), чтобы облегчить кризис стоимости жизни. Правящая коалиция, напротив, предложила одноразовая раздача денег, утверждение о том, что одноразовый платеж будет осуществляться быстрее, и что Доходы от налога необходимы для поддержания системы социального обеспечения страны.

Мужчина в возрасте 20 лет в воскресенье проголосовал в Токио за одну из растущих новых политических партий. выступает за снижение налогов. Благодаря реформе социального обеспечения я ожидаю увеличения заработной платы в нашем рабочем поколении. "

С старением населения в Японии бремя расходов на социальное обеспечение работников стало более тяжелым. По его словам, если у них будет больше дохода, то молодое поколение может потратить больше, и экономика станет более активной. Увы, это будет означать, что Японии, которая уже является самой задолженной страной в мире, нужно будет выпустить еще больше долгов, что сделает еще один раунд монетизации долга QE Банком Японии более вероятным.

Избиратели проголосовали на выборах в верхнюю палату парламента Японии на избирательном участке в Токио 20 июля.

Избиратели проголосовали на выборах в верхнюю палату парламента Японии на избирательном участке в Токио 20 июля. Вопрос налогообложения вышел за рамки традиционной лево-правой политической оси, а сторонники маргинальных партий, таких как левый Рейва Синсенгуми и правый Сансейто, в подавляющем большинстве выступают за сокращение, согласно опросу Nikkei-TV Tokyo в июне.

Казуки Ойкава, мужчина в возрасте 20 лет, сказал, что он голосовал за оппозиционную партию, поддерживая ее экономическую политику. Я надеюсь, что смена правительства вдохнет свежий воздух в японскую политику. Мне не очень понравилось, как ЛДП просто раздавала наличные. "

С другой стороны, 94-летняя женщина Теруко Аоки сказала: Оппозиционные партии говорят только о сокращении налогов и увеличении расходов в эти дни, таких как увеличение пособий по уходу за детьми. Но откуда берутся деньги на все эти сокращения налогов и увеличение расходов? "

Ответ: То же место, куда он придет для финансирования денежных раздач: Больше долгов.

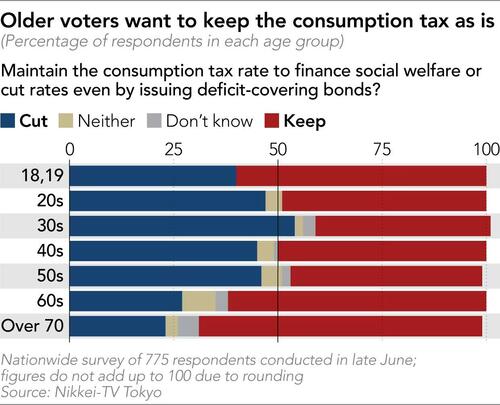

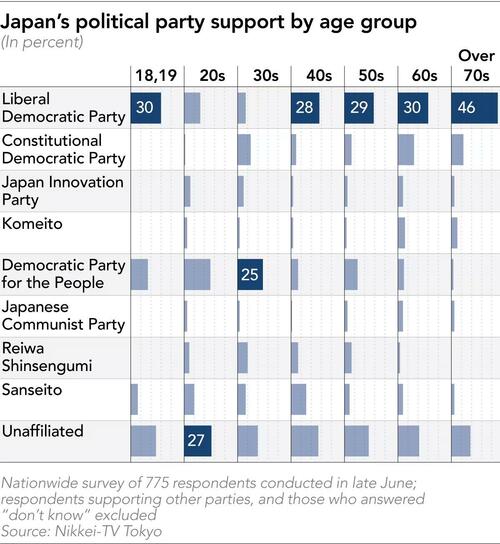

Среди различных возрастных групп люди в возрасте 60-70 лет решительно поддерживают сохранение ставки налога на потребление - 10% для товаров общего пользования и 8% для продуктов питания. ЛДП пользуется самой сильной поддержкой среди пожилых избирателейОпрос показал.

Опасения, что голосование в воскресенье заставит ЛДП пойти на уступки небольшим партиям, рекламирующим политику, которая будет напрягать государственные финансы, привели к распродаже японских государственных облигаций и иены. Доходность по 10-летним японским государственным облигациям достигла самого высокого уровня со времен финансового кризиса 2008 года на прошлой неделе. Доходность на 20, 30 и 40-летних JGB достигает максимума за все время.

Иммиграционная политика также стала ключевой темой кампании, особенно после Сансейто. Выступает за «первую японскую позицию». Завоевал первые места в Токийском метрополитене Выборы в ассамблею в прошлом месяце, в том, что может быть звонком для верхней палаты. Партия выиграла свое первое национальное место на выборах в верхнюю палату 2022 года и имеет три места в нижней палате.

В то время как Япония одновременно продвигала политику приема большего числа иностранных работников и привлечения большего числа иностранных туристов, Япония также активно участвовала в этом процессе. Возникающие в результате этого культурные трения привели к росту опасений по поводу того, как страна может продолжать поглощать приток в будущем (вопрос, который, безусловно, должны задать и политики в Европе).

Многие избиратели чувствуют, что их оттесняют в результате обесценивания иены и роста стоимости жизни за последние несколько лет.

"" На этот раз я хотела проголосовать за партию, больше ориентированную на политику японцев среднего класса, - сказала Юки, 30-летняя женщина, которая не назвала свою фамилию. ""Сейчас японцам очень трудно покупать дома, и наша зарплата не растет. " Многие в США сочувствуют.

Поддержка Sanseito, согласно опросу Nikkei-TV Tokyo, является самой высокой среди тех, кому за 40 лет, группы, которая составляет основную часть так называемого потерянного поколения. Эта когорта начала поиск работы с 1993 по 2004 год, во время экономической стагнации и перенасыщения на рынке труда. Не имея возможности найти стабильную работу, многие из них оказались сотрудниками или фрилансерами.

«В Европе и в США растущее неравенство, иммиграция и проблема беженцев, а также высокая инфляция привели к снижению рейтингов одобрения правительства и проигрышу правящих партий на выборах», — сказал Гокен Суэдзава из Nikko Securities. Он сказал, что национальные выборы в Великобритании, Франции, Японии, США и Германии привели к поражению правящих партий. Ситуация в нашей стране стала напоминать ситуацию в Европе и США.

Сценарии выборов

На выборах в верхнюю палату, 125 из 248 мест могут быть переизбраны (половина мест 124 плюс одна вакансия). Учитывая количество мест в верхней палате и переизбрание / непереизбрание, правящая коалиция имеет 75 мест без переизбрания. Поэтому, Если бы коалиция получила 50 из 66 мест, баллотирующихся на переизбрание, она бы сохранила большинство в верхней палате. Если правящая коалиция получит 49 или меньше мест на переизбрании, она потеряет большинство в верхней палате, как и в нижней палате.

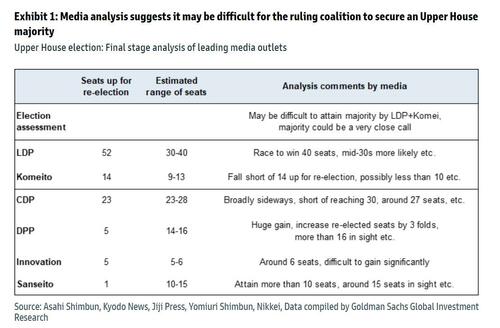

Первоначальные оценки СМИ, сразу после объявления о выборах 3 июля, в значительной степени предполагали, что правящая коалиция ЛДП и Комейто обеспечит большинство, включая невыборные места. Однако в своем недавнем анализе заключительных этапов избирательной кампании СМИ сделали шаг назад. Большинство из них теперь описывают перспективы коалиции ЛДП-Комейто по сохранению большинства как трудные или неопределенные. Многие СМИ предсказывают, что ЛДП получит около 30-40 из 52 мест для переизбрания. «Комейто» выиграет меньше, чем 14 мест.

Сценарии для правительства на основе результатов выборов.

Ниже мы представляем различные сценарии Голдмана для японского правительства в зависимости от результатов выборов в верхнюю палату.

А. Правящая коалиция сохраняет большинство на выборах (выигрывает 50 или более мест переизбрания)

Исиба остается президентом ЛДП, а администрация Исибы продолжает свою деятельность.

Б. Правящая коалиция теряет большинство (выигрывает 49 или меньше мест на переизбрании)

Если правящая коалиция потеряет большинство с небольшим отрывом, администрация Ишибы может продолжить, но для управления парламентом может потребоваться больше пересмотров законопроектов, включающих оппозиционные предложения, чем раньше (необходимо сотрудничать с оппозиционными партиями законопроект за законопроектом).

Исиба уходит в отставку с поста президента ЛДП. Избирается новый президент ЛДП и становится премьер-министром (как и с 1 выше, нужно сотрудничать с оппозиционными партиями).

Если правящая коалиция потеряет большинство с большим отрывом, третья сторона может присоединиться к LDP и Komeito, чтобы сформировать новую администрацию; Учитывая сложность контроля диеты. При этом лидером третьей стороны мог стать премьер-министр.

Кабинет Исибы массово уходит в отставку. Коалиционное правительство формируется действующими оппозиционными партиями.

Либо премьер-министр распускает парламент, либо оппозиционные партии принимают вотум недоверия в отношении кабинета ЛДП/Комея, и проводятся всеобщие выборы в нижней палате. В зависимости от результатов выборов в нижней палате, либо правящая коалиция ЛДП/Комей может сохранить власть, либо оппозиционные партии могут взять власть.

Политика после выборов может иметь экспансионистский фискальный уклон

Диета уже работает с правительством меньшинства, поскольку правящей коалиции не хватает большинства в нижней палате. Многие законопроекты, включая бюджет FY25, были приняты после включения мнений оппозиционных партий. Если коалиция ЛДП-Комейто также потеряет большинство в верхней палате, сотрудничество с оппозицией станет еще более важным для принятия законодательства, даже если администрация ЛДП-Комейто будет продолжать.

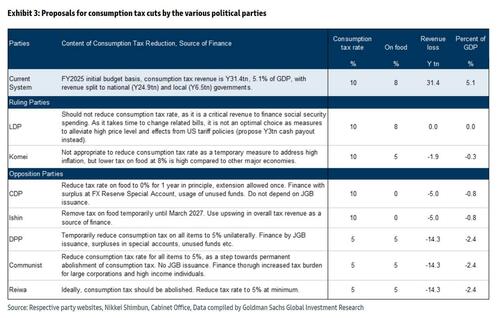

Одним из наиболее актуальных вопросов является инфляция, которая была в центре дебатов во время избирательной кампании в верхней палате. ЛДП заявляет, что Мы не будем сокращать налог на потребление, предлагая вместо этого денежные пособия. превышает в общей сложности 3 трлн иен (0,5% ВВП) в качестве основной инфляционной политики. Эти средства будут финансироваться за счет Увеличение части налоговых поступлений Бюджет FY24.

С другой стороны, почти Все оппозиционные партии призывают к снижению налога на потребление. Однако масштабы предлагаемых сокращений, их продолжительность и источники финансирования сильно различаются (пример 3). В то время как CDP и Японская инновационная партия предлагают временное сокращение на 1-2 года, ограниченное продовольствием и финансируемое без дополнительной эмиссии JGB, DPP предлагает единообразное снижение налога на потребление до 5%. финансируется за счет выпуска JGB.

Сокращение налога на потребление является высоким заказом при действующей администрации, ориентированной на LDP. Это связано с тем, что снижение налога на потребление требует законодательных изменений и других трудоемких процедур, что делает их непригодными для принятия немедленных мер по борьбе с инфляцией. На наш взгляд, было бы также политически трудно вернуться к первоначальной более высокой налоговой ставке только через короткий период, в то время как обеспечение постоянных альтернативных источников финансирования, вероятно, окажется сложной задачей, если сроки для снижения налога на потребление будут продлены.

Тем не менее, экономический пакет, который ЛДП планирует сформулировать осенью, вероятно, будет включать в себя некоторые требования оппозиционных партий, такие как отмена предварительного налога на бензин (1,5 трлн иен), к которому призывают многие оппозиционные партии, и увеличение расходов на уход за детьми и другие области, в дополнение к 3 трлн иен в виде денежных раздач. Более того, как видно из бюджета FY25, коалиция ЛДП-Комейто, как правительство меньшинства, вряд ли сможет принять первоначальный бюджет FY26 (который будет сформулирован к концу 2025 года) без включения некоторых предложений оппозиции, связанных с социальным обеспечением (обслуживание детей, медицинские расходы и т. д.). Таким образом, даже при администрации, ориентированной на ЛДП, мы считаем, что будущее управление политикой неизбежно будет иметь экспансионистскую фискальную предвзятость, при этом все еще принимая во внимание некоторую степень фискальной дисциплины.

В Японии, где дефицит первичного баланса сокращается на фоне роста налоговых поступлений, а бремя процентных платежей на данный момент невелико, краткосрочное снижение налогов или увеличение расходов, которое приводит к увеличению дефицита первичного баланса, вряд ли вызовет рост отношения долга к ВВП в ближайшей перспективе. Однако, согласно нашей модели, предполагающей различные сценарии, постоянное снижение налогов, превышающее 1% ВВП, приведет к постоянному росту соотношения долг/ВВП, подрывая устойчивость государственного долга. Если бы расходы на оборону увеличились до 3% ВВП, практически не было бы места для постоянного снижения налогов.

Вряд ли результаты выборов окажут существенное влияние на денежно-кредитную политику Банка Японии. По мнению экономистов Goldman, маловероятно, что результаты выборов в верхнюю палату окажут значительное влияние на денежно-кредитную политику Банка Японии. Банк Японии обеспокоен риском повышения тарифов, особенно на автомобили. Это может оказать понижательное давление на рост и инфляцию на фоне высокой неопределенности. Поэтому, независимо от результатов выборов, Банк Японии должен Поддерживайте голубиную позицию с точки зрения управления рисками и сохраняйте процентные ставки в течение значительного периода. Если будут введены более высокие тарифы, неясно, будет ли и когда Банк Японии продолжит свое следующее повышение ставок.

** **

Предлагаемые сделки, от торгового стола Goldman:

- Скенарио 1: LDP/Komeito теряет большинство, но занимает место премьер-министра (65%)

В этом наиболее вероятном исходе Голдман рассматривает сценарий, при котором ЛДП/Комейто потеряет большинство, но сохранит премьерство. 1) никакая оппозиция не образует коалицию большинства или 2) третья оппозиционная партия присоединяется к ЛДП/Комейто для формирования нового правительства. Хотя усиление оппозиционного влияния предполагает экспансионистскую фискальную предвзятость, Любые изменения в администрации могут ослабить способность Японии вести переговоры о торговой сделке до истечения крайнего срока 1 августа. В то время как наша макрослужба ожидает, что USDJPY будет торговаться выше, если LDP/Komeito потеряет большинство (что теоретически должно поддерживать рынок акций), политическая неопределенность, вероятно, будет влиять на рынки в ближайшей перспективе. В этом сценарии, Нам нравится широко хеджировать индексы в двоичном двоичном формате (рынок ниже и UDSJPY выше) с окупаемостью 13x max:

Торговые идеи:

- 1/ Купить NKY LOWER/USDJPY HIGHER DUAL BINARY: 12Sep25 NKY100% @ 7.50% Offer, Max PO 13.3x. Убыток Макса - это потраченная премия.

** **

- СКЕНАРИО 2: ЛДП/Комейто сохраняет большинство (25% вероятности)

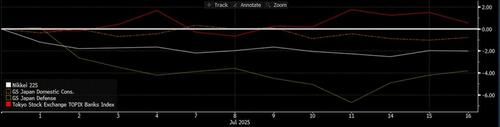

Если LDP/Komeito сохранит большинство («статус-кво»), мы, вероятно, увидим разворот ценового действия MTD. Мы ожидаем, что акциям будет оказана помощь в связи с уменьшением политической неопределенности. На секторальном уровне ключевым бенефициаром, скорее всего, будет оборона (премьер-министр Ишиба поддерживает увеличение расходов на оборону). Что касается торговых переговоров, то этот результат должен иметь относительно более позитивное/нейтральное воздействие, поскольку любое изменение в руководстве, вероятно, вызовет дальнейшие задержки. Банки в последние недели опередили и могут исправить ситуацию.

MTD: NKY, оборона и внутреннее потребление снизились по сравнению с японскими банками

Источник: данные Bloomberg по состоянию на 16 июля25 года. Прошлые результаты не указывают на будущие результаты.

Торговые идеи:

- Купить NKY Calls: NKY 45Sep25 105% Call: 1.25% offer, 19.43v, 22.5d; Убыток Макса - это потраченная премия.

- Купить TPNBNK PUTS: TPNBNK 10Oct25 95%, предложение 3.72%, 28.3v, 36d; Убыток Макса - это потраченная премия.

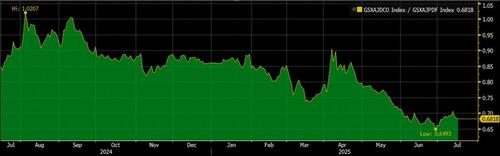

- Защита Японии: GSXAJPDF; Убыток Max на Long TRS является условным + потраченное финансирование. Убыток Max на Short TRS не ограничен.

MTD: NKY, оборона и внутреннее потребление снизились по сравнению с японскими банками

- Скенарио 3: Полное изменение администрирования (10% вероятность)

Хвостовой сценарий, при котором ЛДП/Комейто с большим отрывом теряет большинство, а кабинет Исибы заменяется. Этот сценарий, вероятно, будет иметь негативные последствия для переговоров по тарифам в ближайшем будущем, но будет означать более экспансионистскую фискальную политику в будущем. Кроме того, устранение Исибы будет иметь значительные негативные последствия для расходов на оборону. В этом случае стол любит покупать названия внутреннего потребления, которые выиграют от фискальной экспансии, в сочетании с короткими в обороне для нейтральной реализации на чистом рынке.

Торговые идеи:

- Покупка японского домешника: GSXAJDCO (Max loss on Long TRS is conceptal + financing spent). Убыток Max на Short TRS не ограничен.

- Защита Японии: GSXAJPDF (Max loss on Long TRS is conceptal + financing spent). Убыток Max на Short TRS не ограничен.

Долгое внутреннее потребление и короткая оборонная торговля должны измениться, если мы увидим полную смену администрации.

Тайлер Дерден

Солнце, 07/20/2025 - 10:15