NIRP возвращается, поскольку Национальный банк Швейцарии снижает ставки до нуля, вводя отрицательные ставки

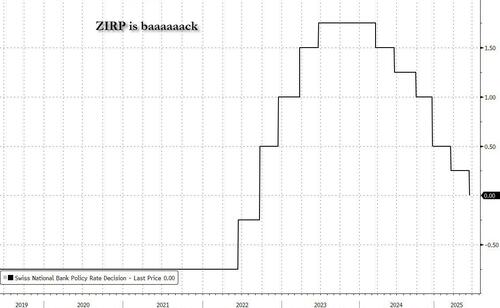

Через пять лет после того, как Ковид спровоцировал Один раз в поколение Инфляционный всплеск и заставил все центральные банки поднять свои процентные ставки значительно выше нулевой (а в некоторых случаях отрицательной) нижней границы, которая определила эпоху после QE, в одночасье Швейцарский национальный банк стал первым, кто показал, что мир более высоких ставок закончился, и ZIRP возвращается, после того как центральный банк снизил свою ставку с 0,25% до 0,00% впервые с 2022 года.

Но не только ZIRP возвращается. NIRP также здесь благодаря швейцарцам, потому что, хотя SNB, возможно, снизил свою процентную ставку до нуля, он наказывает избыточные резервные запасы банков. Кредиторы столкнутся с отрицательными ставками, если они припаркуют слишком много денег в центральном банке.

Да, магия нулевой нижней границы снова с нами!

Согласно заявлению SNB, опубликованному в четверг утром, швейцарские банки могут держать свои минимальные резервные депозиты в SNB бесплатно до 18 раз. все, за что они будут взиматься проценты -0,25% Скидка по ставке остается неизменной на уровне 25 базисных пунктов.

Цель «уровня вознаграждения», по данным Bloomberg, состоит в том, чтобы стимулировать кредитование между банками. На швейцарском денежном рынке обменивается достаточно ликвидности. Для кредиторов, держащих больше своего лимита, дешевле передать избыточные резервы учреждениям, которые находятся под их порогом, потому что они должны платить им меньше, чем центральный банк.

Для всех кредиторов, которые не имеют минимального резервного требования, порог установлен на ничтожных депозитах в размере 10 миллионов франков ($12 миллионов).

Система, которую SNB установил с тех пор, как он поднял ключевую ставку выше нуля в 2022 году, означает, что средняя ставка денежного рынка, известная как Сарон, обычно была на несколько базисных пунктов ниже ставки центрального банка.

Это означает, что начиная с пятницы, Поэтому вероятны отрицательные затраты на финансирование банков. Об этом в качестве члена правления Петра Цчудин рассказала журналистам в Цюрихе. Она добавила, что ожидает, что только «очень маленькие» депозиты будут вознаграждаться по отрицательной ставке. Это перекликается с опытом работы в течение примерно трех лет при режиме, когда, как правило, только небольшая часть из них пострадала от более низкой ставки.

Тем не менее, мало или не так мало, отрицательные ставки возвращаются, по крайней мере, в одной стране. И вскоре во многих других.

Хотя основное банковское лобби Швейцарии назвало решение SNB «понятным», оно подвергло критике его последствия.

Очевидно, что нулевая процентная ставка снижает стимул к ответственным сбережениям и оказывает дополнительное давление на пенсионное обеспечение. Об этом говорится в заявлении Швейцарской ассоциации банкиров. "Как и в предыдущие периоды низких процентных ставок, банки и их клиенты вновь несут значительную долю бремени денежно-кредитной политики. "

Аналогичным образом, страховая ассоциация приветствовала то, что SNB не стал отрицательным, но подчеркнула, что «даже возвращение к низким процентным ставкам уже создает проблему» для сектора.

СНБ Президент Мартин Шлегель признал дискомфорт, создаваемый новой ценовой конъюнктурой для банков, и дал понять, что для дальнейших сокращений существует повышенная планка.

«Мы бы не приняли решение идти негативно», — сказал он. «Но я хочу подчеркнуть, что прибыльность банков не входит в задачи национального банка. "

Наконец, в то время как некоторые утверждают, что отрицательные ставки являются способом для центральных банков с дефицитом капитала пополнить свою казну после того, как годы высоких ставок подтолкнули их всех к технической несостоятельности, учитывая небольшую долю затронутых депозитов, маловероятно, что SNB будет зарабатывать много денег от взимания платы с кредиторов. В период с 2015 по 2022 год центральный банк заработал почти 12 миллиардов франков от отрицательных ставок, хотя затем выплатил 14,5 миллиардов франков, когда ставки стали положительными до конца марта этого года.

Тайлер Дерден

Thu, 06/19/2025 - 17:10