Что такое «Тихий день»?

Исполнитель: Michael Every Of Rabobank

Не было никакого "Тихие дниВ 2025 году в глобальной стратегии будет наблюдаться постоянный поток взаимосвязанных событий в геополитике и геоэкономике. Последние 24 часа не стали исключением.

Израиль нанес удар по лидерам ХАМАСа в Дохе, Катар, который, возможно, — неподтвержденный — убил их переговорную команду; или, по крайней мере, тех, кто вчера отказался от «окончательной» сделки Трампа, через 24 часа после того, как он предупредил, что будут последствия, если она будет отклонена. Это вызвало опасения по поводу региональной заразы, но у Катара, который уже подвергся нападению со стороны Ирана в начале года, нет собственных реальных вооруженных сил, только крупнейшая авиабаза США на Ближнем Востоке.

Международное осуждение было быстрым. Даже Трамп выступил в оппозиции, заявив, что он не знал о нападении до последнего момента и пытался предупредить Катар (который должен был быть в состоянии обнаружить его сам; и турецкие источники утверждают, что он не знал о нападении до последнего момента). они Доху и Хамас отключили. Трамп добавил, что его следует использовать в качестве платформы для мира и что он будет углублять оборонные отношения с Катаром в будущем. Во всем этом есть слои ошибочных представлений, искажений и потенциальных ошибок, но это предполагает дальнейшие сдвиги в регионе - мы посмотрим, идет ли речь о мире или большем конфликте.

Между тем, пока Европа спала, российские (иранские) беспилотники совершили массовую атаку на Украину, а также вошли в воздушное пространство Польши, увидев, что несколько самолетов F-35 стран ЕС поднялись в воздух, а польские аэропорты приблизились к Варшаве. Один из представителей США опубликовал:

"Россия нападает на союзника НАТО Польшу... Это акт войны, и мы благодарны союзникам по НАТО за их быстрый ответ на продолжающуюся неспровоцированную агрессию военного преступника Путина против свободных и продуктивных стран. Я призываю президента Трампа ответить обязательными санкциями, которые обанкротят российскую военную машину и вооружат Украину оружием, способным нанести удар по России. Путин больше не довольствуется тем, что просто проигрывает на Украине во время бомбардировок матерей и младенцев, он сейчас напрямую проверяет нашу решимость на территории НАТО. Путин заявил, что «Россия не знает границ». Свободные и процветающие страны будут учить Россию границам. "

Действительно, в то время как Трамп ранее продолжил разрядку в американо-индийском интернете, опубликовав пост, в котором он по-прежнему ожидает, что торговая сделка будет согласована, он тогда сказал Европе, что она должна ввести 100% тарифы на Китай и Индию, чтобы остановить Путина, за которым он последует. Сказать, что это имеет серьезные последствия, - это преуменьшение: большинство из них, если это сделано, но также, если это не так - Потому что это даст понять, что ЕС (и США) не готовы использовать достаточно сильные экономические методы государственного управления, что оставляет их либо с военными методами государственного управления, либо без них. Жирный хвост рискует на обоих.

В то же время Непал только что потерял своего премьер-министра после жестоких общественных протестов, когда его парламент сгорел - крошечное государство, зажатое между гигантской Индией и Китаем, находится в центре их (и других) внимания.

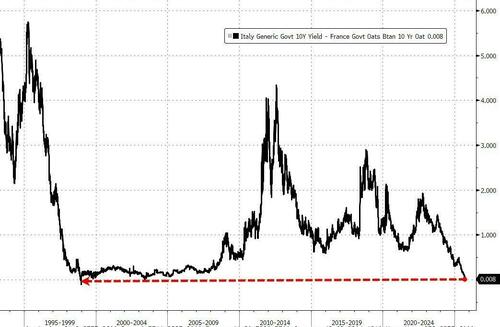

Президент Франции Макрон назначил 39-летнего Министр обороны Лекорну в качестве своего последнего премьер-министра... Как долго он продержится Расходы на французские заимствования сейчас занимают первое место в Италии, что Bloomberg называет «историческим сдвигом на рынке».? И кто остался «ядром» еврозоны по сравнению с «периферией», и какой процент ВВП еврозоны они представляют? Я прошу друга из центрального банка.

Индонезия, также столкнувшаяся с крупными общественными протестами - дом министра финансов был сожжен до того, как они ушли в отставку - видела, как ее президент попросил центральный банк напрямую снизить стоимость заимствований для ключевых проектов своего администратора. По крайней мере, это отвечает на вопрос: «Что такое ВВП? "

В этом геоэкономическом водовороте Китай стремится укрепить связи АСЕАН, сообщает SCMP, что "В преддверии 22-й Китайско-АСЕАН на следующей неделе Представитель министерства торговли ЭКСПО заявил, что торговые партнеры могут официально обеспечить более тесные экономические связи в этом году". Таким образом, более крупный торговый дефицит АСЕАН с Китаем будет тогда, и США не позволят перевалке отправлять эти товары своим путем. Тем не менее, у Европы нет таких барьеров, и если она их поднимет, она снова перейдет в торговый блок США, как мы прогнозировали.

В чисто экономических новостях, как будто в настоящее время может быть что-то подобное, FT говорит, что Рэйчел Ривз должна сказать министрам, чтобы они расставили приоритеты в борьбе с инфляцией в Великобритании, поскольку депутаты от лейбористов вместо этого «все больше обеспокоены» навязанной экономической политикой. " Разве мы не видим «снижения ставок»?

Аналогичным образом, WSJ сообщает, что «инфляция в прошлом году привела к снижению доходов в США», поскольку «домохозяйства с высоким доходом жили лучше, чем другие, в то время как женщины потеряли почву для мужчин». Это не похоже на то, что главная улица бьет Уолл-стрит.

Кроме того, пересмотр данных о заработной плате в США в сторону понижения на -911K в марте 2025 года, который представляет совершенно иной прогноз для экономики, чем ранее, и, как я отметил несколько недель назад, Остается только гадать, почему мы удосужились взглянуть на эти данные — помимо месячной рутины казино выше / ниже, чем это есть. Bloomberg также 1/3 лучших рабочих мест в BLS в настоящее время не заполнены, что не означает, что качество данных скоро улучшится. Но, эй, более широкий, более дикий диапазон результатов в ежемесячном казино, верно? ВП Вэнс написал: «Трудно переоценить, насколько бесполезными стали данные BLS. Изменения необходимы для восстановления доверия. "Но изменить что?

Более того, американский судья постановил, что обвинения в мошенничестве с ипотекой, отправленные в Министерство юстиции, по-видимому, не являются необходимыми «для дела» или уведомления, чтобы Трамп уволил ее, поэтому губернатор Кук может остаться на работе на встрече FOMC на следующей неделе. Опять же, ожидайте, что это будет обжаловано и / или в конечном итоге в Верховном суде, где некоторые подозревают, что это будет отменено в рамках расширения исполнительной власти над государственными служащими (так называемый исполнитель Хамфри). Тем временем, Кук, голубь, собирается голосовать за снижение ставки или вдруг станет ястребом, несмотря на пересмотр зарплат?Кто знает, но политика и политика личности в центральном банке? Кто бывало?

Кроме того, Верховный суд США также согласился рассмотреть тарифную апелляцию Трампа в IEEPA в ноябре.

На рынках Anglo American и Teck должны объединиться, создав гигант по добыче меди с рыночной стоимостью более 53 миллиардов долларов. Учитывая, насколько важна медь для энергетических систем, что имеет решающее значение для ИИ, что имеет решающее значение для национальной безопасности, и любые надежды на то, чтобы вытащить нас из нашего высокого долга, высокой инфляции, низкого падения производительности, очевидно, не будут подвергаться какому-либо экономическому давлению со стороны США или Китая. Честный. Все это будет «потому что рынки». "

Китай предлагает финансирование исследований стейблкоинов по мере роста глобального интереса, где крупнейшее государственное исследовательское бюро страны предлагает гранты для изучения цифровых активов. Как контролировать свои движения" Может ли это иметь какое-то отношение к надвигающемуся введению стейблкоинов в долларах США и их способности де-факто долларизировать другие экономики?

Как я уже сказал, это далеко не тихо. Некоторые сообщения кричат так громко, как только могут, даже если они искажаются по объему.

Тайлер Дерден

Свадьба, 09/10/2025 - 12:20