Почему экономические теории Кейнса провалились в реальности

Автор Лэнс Робертс через RealInvestmentAdvice.com,

Недавняя статья Даниэля Лакалла "Как кейнсианцы снова ошиблись в экономике США Обнаружен растущий разрыв между экономической теорией Джона Мейнарда Кейнса и реальностью. Несмотря на уверенные прогнозы ведущих кейнсианских экономистов, экономика США в 2025 году продолжает игнорировать ожидания. Ужесточение Федеральной резервной системы не смогло запустить широко предсказанный цикл. жесткая посадка«И рост оказался более устойчивым». Одновременно инфляция остается несколько липкой, но все еще снижается, и экономика отказывается следовать аккуратным, линейным путям, которые предлагают модели учебников.

Это последнее смущение для ортодоксии Кейнса является частью гораздо более широкой истории. Провалы — это не отдельные просчеты, а предсказуемый результат ошибочной структуры, к которой политики цеплялись десятилетиями. Кейнсианская экономика не только «Ошибитесь» В 2025 году, но уже более сорока лет не выполняет своих обещаний. И последствия становится невозможно игнорировать.

По своей сути кейнсианская экономика обманчиво проста. Когда спрос на частный сектор падает, правительство должно заимствовать и тратить, чтобы заполнить этот пробел. Идея заключается в том, что временные инъекции фискальных стимулов сгладят бизнес-циклы, уменьшат безработицу и быстро вернут экономику на полную мощность.

Ключевое слово здесь - временный. Джон Мейнард Кейнс (John Maynard Keynes) ясно дал понять, что правительства должны иметь дефициты во время спадов и профициты во время экспансии. Долг, понесенный для спасения экономики, должен быть погашен после нормализации условий.

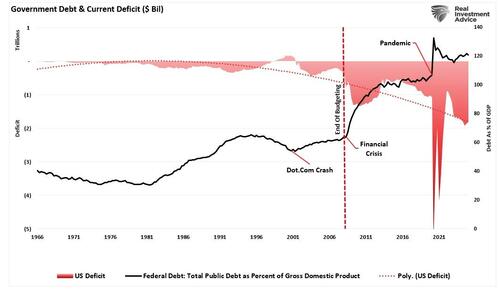

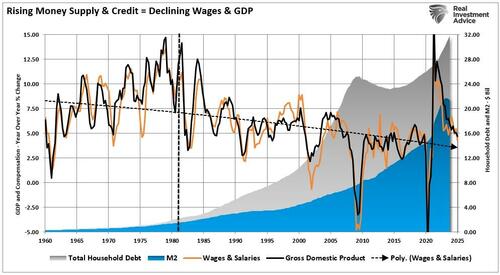

Однако на практике эта дисциплина так и не материализовалась. Политики обнаружили, что избиратели любят стимулы, но ненавидят меры жесткой экономии. С 1970-х годов дефицит стал постоянной чертой фискальной политики США, независимо от бизнес-цикла. Результаты отрезвляют: государственный долг США в настоящее время превышает 120% ВВП, программы социальных пособий структурно недофинансированы, и каждый кризис требует более масштабных вмешательств с уменьшающимися экономическими выгодами.

Пандемия COVID-19 была последним экспериментом Кейнса. Между 2020 и 2022 годами федеральное правительство ввело $5 трлн. В дополнение к фискальному стимулированию экономики Федеральная резервная система снижает процентные ставки до нуля и расширяет свой баланс на 120 миллиардов долларов каждый месяц. Согласно кейнсианской модели, этот беспрецедентный монетарный и фискальный стимул должен был привести к устойчивому экономическому буму.

Неудача искусственного роста

Однако, как мы отметили в «ММТ пытались и потерпели неудачу»Массовый поток стимулов временно стимулировал экономический рост. «Движение вперед» Будущий спрос, но и он создал несколько проблем.

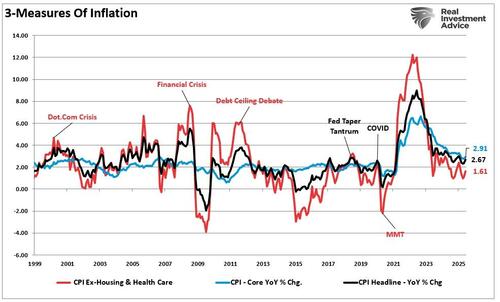

«Наиболее очевидной проблемой является влияние резкого увеличения спроса на экономику, страдающую от нехватки предложения. Поскольку экономика «затормозилась» из-за правительственных ограничений, поток стимулирующих платежей привел к росту спроса. Учитывая базовую экономику спроса и предложения, цены выросли. Как и ожидалось, реализация привела к массовому всплеску инфляции. (Учитывая, что большинство американцев имеют фиксированные выплаты по здравоохранению и жилью на договорный период, третья мера показывает, какая стоимость жизни для большинства каждый месяц).

Важно отметить, что инфляция, за исключением жилья и здравоохранения, выросла почти до 12% во время всплеска расходов, вызванных пандемией. Однако сегодня, когда экономика замедляется, а стимулы исчезают из системы, уровень инфляции снизился до 1,61%.

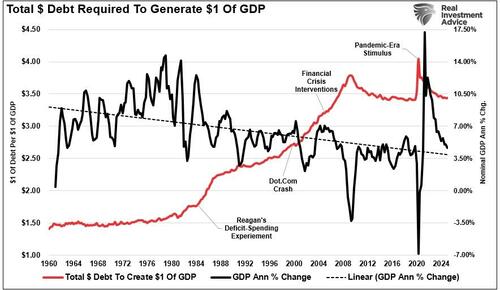

Во-вторых, «Экономический бум» Стимулы, вызванные стимулированием спроса, продолжают исчезать, поскольку экономика постепенно нормализуется до примерно $3,50 долга, чтобы заработать $1 экономической активности. После прекращения пандемии экономика выросла до беспрецедентных уровней, приблизившись к номинальному росту в 17,5%. В закрытой экономике побочным продуктом всего этого спроса был всплеск инфляции. 40-летние максимумыПик выше 9% в 2022 году. Пять лет спустя инфляция продолжает снижаться к целевому показателю ФРС в 2%, но остается липкой, поскольку остатки монетарного и фискального стимулирования продолжают проходить через систему.

Сломанная передача денежно-кредитной политики

Дальнейшим провалом современной кейнсианской политики является ее чрезмерная зависимость от центральных банков. Благодаря снижению ставок и количественному смягчению (QE) денежно-кредитное стимулирование стало решением для любого экономического спада. И все же передающий механизм Между денежно-кредитной политикой и реальной экономической деятельностью фундаментально нарушена. Искусственные вмешательства и "ММТ" На самом деле это не сработало, потому что основная система передачи не сработала.

«Обещание чего-то ни за что никогда не потеряет своего блеска. Поэтому ММТ следует рассматривать как форму политической пропаганды, а не как реальную экономическую или государственную политику. И, как и всякая пропаганда, мы должны бороться с ней призывами к реальности. ММТ, где дефицит не имеет значения, является нереальным местом. "

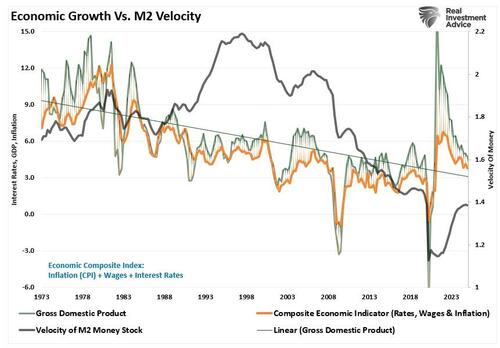

Между тем, Скорость денегТемп, при котором деньги переходят из рук в руки в экономике, в то же время восстанавливаясь после экономического спада, продолжает снижаться. Другими словами, ФРС может вводить ликвидность, но не может эффективно циркулировать. Тенденция скорости не дает обнадеживающих перспектив для роста ВВП.

С учетом ослабления темпов экономического роста и последующего снижения инфляции, что является прямым отражением ослабления потребительского спроса, у банков мало стимулов для расширения кредитования по текущим ставкам, особенно в условиях ужесточения регулирования и низкого качества кредитования.

Одна из ключевых проблем заключается в том, что кейнсианские модели предполагают линейную причинно-следственную связь между государственными расходами и экономическим производством. Они почти полностью сосредоточены на совокупный спрос, пренебрегая критической динамикой, такой как насыщение долга, хрупкость цепочки поставок и циклы обратной связи на глобальных рынках капитала.

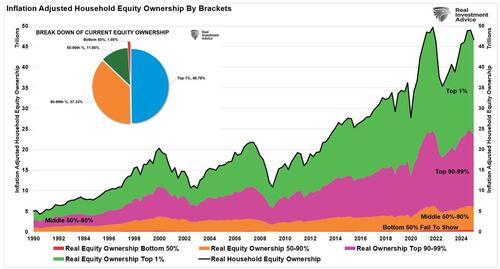

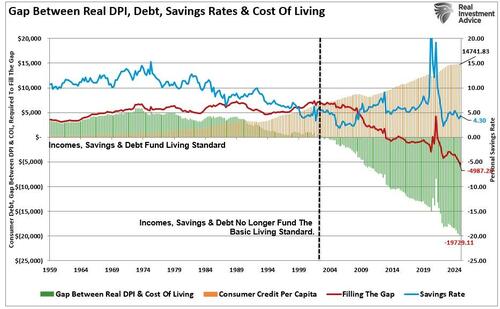

В современной высоко финансиализированной экономике государственные расходы не циркулируют эффективно. Как уже отмечалось, большая его часть попадает в ловушку финансовых рынков, раздувая цены на активы, а не стимулируя продуктивные инвестиции. Ультранизкие процентные ставки, еще одна отличительная черта кейнсианской политики, препятствуют сбережениям и поощряют спекуляцию, подпитываемую долгами. Это искажает распределение капитала, вызывая неэффективные инвестиции в непродуктивные активы, такие как акции мемов, спекулятивная недвижимость и убыточные технологические предприятия. Большинство льгот остаются в ловушке в топ-10 процентов экономики, которая владеет примерно 88% финансовых активов с поправкой на инфляцию.

Другими словами, богатые сохраняют денежные вливания, в то время как инфляция облагает их налогами.

Г-н Лакалли подчеркнул это несоответствие между теориями Кейнса и экономическими реалиями. Как он отметил, многие ведущие экономисты неоднократно прогнозировали рецессию 2023-2024 годов, которая так и не наступила, недооценивали сохранение инфляции и неправильно понимали влияние ужесточения налогово-бюджетной политики. Эти ошибки в прогнозировании выявляют более глубокие недостатки в том, как кейнсианцы моделируют современную экономику.

Предупреждения Хайека доказывают пророчество

Австрийская школа экономики, особенно взгляды Фридриха Хайека, резко контрастирует с кейнсианским мышлением. Австрийские экономисты считают, что Устойчивый период низких процентных ставок и чрезмерное кредитование создают опасность.Дисбаланс между сбережениями и инвестициями. Другими словами, низкие процентные ставки, как правило, стимулируют заимствования из банковской системы, что приводит, как и следовало ожидать, к расширению кредита. Это расширение кредита, в свою очередь, увеличивает предложение денег.

Поэтому, как и следовало ожидать, Бум, связанный с кредитами, становится неустойчивым, поскольку искусственно стимулируемые заимствования стремятся к уменьшению инвестиционных возможностей. Наконец, кредитный бум приводит к широкомасштабным неэффективным инвестициям. Когда экспоненциальное создание кредита больше не является устойчивым, «кредитное сокращение» Это происходит, в конечном итоге сокращая денежную массу. Рынки в конечном итоге «проясняются», что приводит к перераспределению ресурсов в сторону более эффективного использования.

Современные политики отказываются допустить этот естественный процесс. Каждый спад приводит к более агрессивному стимулированию, что только задерживает необходимые корректировки. Результатом стало неуклонное наращивание экономических дисбалансов. Неэффективные компании выживают на дешевых долгах, зомби-фирмы множатся, а инновации страдают. Каждая экономическая экспансия слабее предыдущей, и каждое восстановление зависит от более масштабных интервенций.

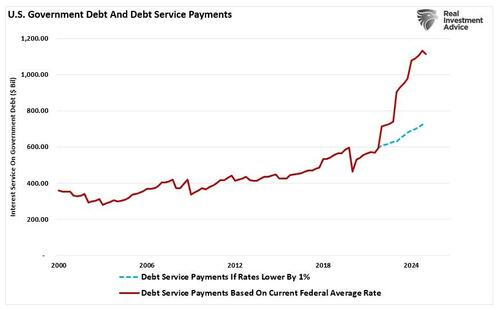

Возможно, самое большое заблуждение, увековеченное кейнсианскими экономистами, заключается в том, что стимулирование, финансируемое за счет долга, является бесплатным обедом. На самом деле обслуживание долга и рост расходов на обслуживание долга становятся значительным экономическим встречным ветром. Бюджетное управление Конгресса прогнозирует, что процентные платежи США превысят расходы на национальную оборону в ближайшие годы. 1,5 триллиона долларов в год К 2030 году. Конечно, это предполагает, что ставки остаются там, где они находятся в настоящее время. Следующий кризис, который стал более распространенным с начала века, значительно снизит ставки. Как показано, снижение ставок на 1% существенно повлияет на будущие обязательства.

Это не просто фискальная проблема, это макроэкономическое сопротивление. Расходы на выплаты процентов отвлекают их от инфраструктуры, образования или продуктивных инвестиций. Хуже того, рост уровня задолженности вытесняет частные инвестиции, искажает рынки капитала и снижает гибкость реагирования на будущие кризисы.

Вывод: экономическая теория Кейнса провалилась

В течение последних 40 лет каждая администрация и Федеральная резервная система продолжали работать в рамках денежно-кредитной и фискальной политики Кейнса, полагая, что модель сработала. Реальность, однако, заключается в том, что большая часть совокупного роста экономики финансируется за счет дефицитных расходов, кредитной экспансии и сокращения сбережений.

Это сократило производительные инвестиции и замедлило производство в экономике. Поскольку экономика замедлилась, а заработная плата упала, потребитель взял на себя больше рычагов, уменьшив сбережения. Результат увеличения левериджа потребовал больше доходов для обслуживания долга, а не топлива для увеличения потребления.

Во-вторых, большинство программ государственных расходов перераспределяют доходы от рабочих на безработных. Экономисты Кейнса утверждают, что это увеличивает благосостояние многих пострадавших от рецессии. Что игнорируют модели Это снижение производительности, которое следует за перераспределением ресурсов и отходом от производственных инвестиций.

Все эти вопросы повлияли на общее процветание экономики. Наиболее показательной является неспособность нынешних экономистов, которые поддерживают нашу денежно-кредитную и фискальную политику. Чтобы понять проблему попытки «излечить проблему задолженности за счет увеличения задолженности. "

Вот почему экономическая политика Кейнса потерпела неудачу. «Наличные для клюкеров» то "Количественное смягчение. " Каждое вмешательство либо тянуло будущее потребление вперед, либо стимулировало рынки активов. Оттягивание будущего потребления вперед оставляет "лишние" В будущем он должен быть постоянно заполнен. Однако создание эффекта искусственного богатства уменьшает сбережения, которые могут быть использованы для продуктивных инвестиций.

Пришло время проснуться и понять, что мы на одном пути.

Тайлер Дерден

Фри, 09/05/2025 - 13:05